The Morning Meeting with Al Tompkins is a daily Poynter briefing of story ideas worth considering and other timely context for journalists, written by senior faculty Al Tompkins. Sign up here to have it delivered to your inbox every weekday morning.

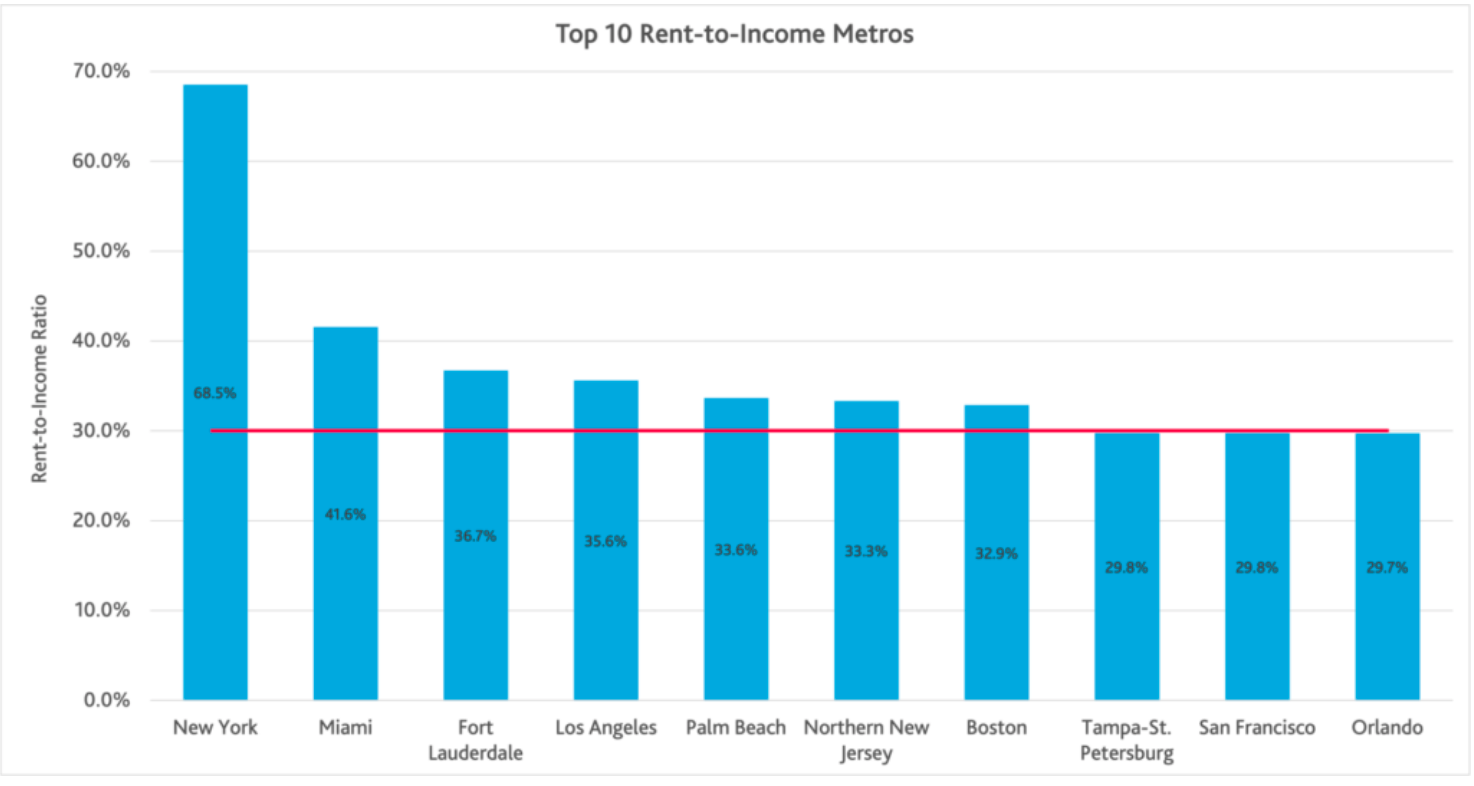

The percentage of a household’s income that goes toward rent is referred to as the rent-to-income ratio. In the United States, the national average rent-to-income ratio just hit a 20-year high. Moody’s Analytics says:

The national average rent-to-income (RTI) reached 30% for the first time in our 20+ years of tracking history, up 1.5% from year-ago or 0.2% from Q3, keeping the growth rate constant throughout the second half of last year.

Rising mortgage rates caused many households to be priced out from home buying and would-be buyers to remain renters. Apartment demand surged as a result and drove rates sky high. As the disparity between rent growth and income growth widens, Americans’ wallets feel financial distress as wage growth trails rent growth.

(Moody’s Analytics)

The stress from rental costs is experienced differently around the country. Moody’s says some states saw a recent drop in average rent costs:

At the state level, three states topped the 30% rent-burdened threshold similar to Q3: Massachusetts (32.9%), Florida (32.6%), and New York (31.2%).

Over the past three years, Nevada (+4.9%), Florida (+4.8%), Alabama (+4.2%), South Carolina (+4.2%), Arizona (+4.1%), and New Mexico (4.0%) all experienced the highest increase in the state’s average rent burdening, attributed to significantly higher (>~20%) rent growth than respective median household income growth during the three-year period.

In 2022, five states’ rent-to-income ratios dropped: Maryland (-0.62%), Oklahoma (-0.49%), Arkansas (-0.16%), Minnesota (-0.08%), and Utah (-0.02%).

In Q4, nine states (Georgia, Maryland, Oklahoma, Nevada, Utah, Wisconsin, Pennsylvania, Texas, and Alabama) found some relief in rent burdening, among which Georgia (-1.7%) and Maryland (-1.2%) both recorded average rent decline at the state level.

(Axios)

Realtor.com says there are good reasons to expect that rental prices will cool off this year:

The deceleration from recent highs is consistent with what we have seen in recent for-sale data, suggesting that more typical seasonal cooling is returning to the rental market.

Despite the winter slowdown, Realtor.com forecasts rent growth to continue in 2023 but at a slower pace.

On the demand side, rising housing costs resulting from high mortgage rates may keep more potential buyers in the rental market for longer as consumer home-buying sentiment remains low even after this month’s uptick. In addition, slowing new residential construction could also put off home shopping plans and further increase rental demand.

On the supply side, the number of for-rent properties may gradually increase as homebuilding activity continues to pivot to multi-family properties. This extra supply in multi-family homes could shift market balance, raising the still-low rental vacancy rate and helping temper recent rent growth driven by the excess demand.

- The median asking rent in the 50 largest metros declined to $1,712, down by $22 from last month and $69 from July’s peak.

- Rents in Sun Belt metros slowed to 0.9% Y/Y. Jacksonville, FL (-0.8%) and Austin, TX (-0.6%) experienced their first year-over-year dip in at least 20 months.

- Faster rent growth in the Midwest market such as Indianapolis, IN (9.6%) and Kansas City, MO (8.7%) could raise affordability concerns.

- Rent growth keeps cooling for all unit sizes. Rent by size: Studio: $1,446, up 5.9% ($81) year-over-year; 1-bed: $1,596, up 3.2% ($49); 2-bed: $1,877, up 2.6% ($48).

See the latest apartment rental prices in the 50 biggest metro areas of America here.

The cost of living is contributing to Japan’s population crisis

For the first time in more than 120 years, Japan will record fewer than 800,000 births this year, the country’s ministry of health says. That’s a problem because Japan also has one of the world’s longest life expectancies. In short, the country is getting older and not enough young people are coming up to sustain the future.

Young people cite a couple of major factors for not having children, including the lack of affordable child care and the high cost of housing.

Read more from CNN, Reuters, Wilson Center, NHK and NikkeiAsia.

The doomsday clock moves closer to midnight

The Bulletin of the Atomic Scientists keeps the “doomsday” clock, which symbolizes how precariously close the group thinks that humankind is to a nuclear war. Largely because of the Russian invasion of Ukraine and the uncertainty over Russia’s intentions, the group moved the clock up 10 seconds, which is the closest to “doomsday” the clock has ever been.

The clock has been sitting on 100 seconds until midnight since January 2020 and now is at 90 seconds before midnight. It is not just the war in Ukraine that moved the clock forward but also the climate crisis, cyber threats, biological threats and North Korea’s nonstop nuclear weapon testing.

“We are living in a time of unprecedented danger, and the Doomsday Clock time reflects that reality,” said Rachel Bronson, president and CEO of the Bulletin of the Atomic Scientists. The group added:

Russia’s invasion of Ukraine has increased the risk of nuclear weapons use, raised the specter of biological and chemical weapons use, hamstrung the world’s response to climate change, and hampered international efforts to deal with other global concerns. The invasion and annexation of Ukrainian territory have also violated international norms in ways that may embolden others to take actions that challenge previous understandings and threaten stability.

See a video of the virtual press conference.

Lab-grown diamonds are gaining popularity

The Economic Times (of India) is among several news outlets proclaiming the popularity of lab-grown diamonds is disrupting the diamond industry. It is an interesting story to consider as Valentine’s Day approaches. BusinessWire reports that the synthetic diamonds industry is a $14 billion business in the United States and is expected to continue growing 8% a year for the next seven years.

There is a substantial gap in cost between natural diamonds and manufactured industrial diamonds. Synthetic diamonds can be purchased for as little as US$ 800 per carat all the way up to US$ 1000 per carat, according to the industry standard.

At this time, approximately 1% of the market for diamond jewelry worldwide is held by synthetic diamonds. Despite this, it is anticipated that the use of synthetic diamonds in the production of jewelry will expand as a result of the ongoing research and development in the technology required for the production of synthetic diamonds.

The story behind how diamonds became a “must-have” for brides is a story of advertising genius.

Hertz starts offering electric cars to rent

A week ago, when I rented a car in Nashville, I was surprised to see how many electric cars Hertz had on the lot. Axios says Hertz just announced plans to buy 100,000 electric cars from Tesla, 175,000 from GM and 65,000 from Polestar.

Even though fewer cars were bought in the United States in 2022 compared to the year before, marking a decline for the first time in over a decade, more of these vehicles were electric. US passenger vehicles fell in 2022, but the number of EVs went up by a remarkable 65 percent, an increase of almost two thirds compared to 2021.

EVs accounted for 5.8 percent of all new cars sold in the US, an increase from 3.1 percent the year before.

Projections say the number of electric vehicles sold in the US will surpass the 1-million mark in 2023. And keep in mind this will be sales of mostly expensive vehicles as the selection of affordable EVs won’t dramatically increase this year.

The average price of an EV sold in the US last year was $61,448, a 5.5 percent decrease compared to 2021.

No-filter selfies are out, mirrors are in. Please keep up.

Life is moving pretty fast, so please try to keep up. The #nofilter selfie trend is toast and now the cool people are buying mirrors for their selfies.

Glad I could help.